The Largest Arbitrage in Technology

Updating my prior assumptions on AI-enabled rollups

Just over a year ago I jotted down some thoughts about a pattern I was seeing: venture investors backing software companies to acquire their customers. The idea has caught fire – now branded ‘AI-enabled rollups’ with nearly every Tier 1 venture fund circling the table. Publicly, we’ve seen dedicated vehicles and a quiet second wave is forming in private:

Over the past year, I’ve had the privilege of working with and swapping notes with operators who are stitching these platforms together, and decided to sit down and update my preliminary thoughts with some of the lessons we’ve learned.

Does the Right Capital Exist?

The appeal of AI-enabled rollups is clear:

AI has reduced barriers (ie development costs) to building software, so distribution is theoretically more valuable.

Agentic software can execute full workflows. If you are selling this software with seat-based pricing, you’re leaving value on the table.

Selling software to legacy industries (particularly in SMB categories) has traditionally been difficult for adoption reasons and the deal sizes are usually too small to make the sales effort worthwhile.

If you can truly create transformative software, you capture more value using that tool to run the "end" business than you do selling that tool to others

There is a lot of dry powder that must be deployed, and the rollup strategy allows for chunkier cheques to be written

Despite these reasons—which has made this playbook became a self-propagating meme across so many firms—many folks strongly believe that venture is the wrong equity to fund these rollups. Andrew Ziperski brought forward some good arguments last year; Nathan Benaich and Nikola Mrkšić also put together some strong thoughts at the end of June.

When Venture Works

I’m partial to Slow Ventures’ Growth Buyout (GBO) thesis: if the software is the primary engine of value creation and the acquisitions are merely a way to lock in distribution, data or margin capture, venture math can work. You need to have a really ‘product’ edge to justify venture dollars. There are many categories where I think this is possible today, but there are many more where I’m not convinced technology adds enough value.

Think of each VC dollar as either doing (a) building the platform or (b) buying assets. The more it flows to (a) — R&D, integration tooling, playbooks — the closer you are to classic venture risk/return. When most of the round tilts to (b), cheaper, longer-dated capital is usually the better match.

The Dilemma: Compounding Takes Time

While we don’t have a full cycle case study for this playbook, vanilla rollups have been around for the better part of the last century.

A simpler question is to strip away the AI-effect, and ask whether or not top tier consolidation platforms can generate venture-scale returns. If we could write a US$10M cheque into one of the top-performing consolidation platforms of the past 30 years, would that single position have delivered true venture-scale returns?

Constellation Software (CSI) is as good of a case study as any. For those unfamiliar, CSI is a rollup of vertical market software (VMS) businesses. Since 1995, the firm has completed over 1,000 acquisitions across six operating groups, compounded shareholder capital at over 20% for three decades, and is now valued at north of $100B (CAD).

Impressively, Mark Leonard raised $25M CAD in 1995 and never raised another cent in equity. Their 2006 IPO was purely secondary, so we don’t need to consider dilution in this analysis.

Here’s how it would play out if you invested $1OM USD in this round:

The VC would walk away with $77.5M CAD — a very respectable 5.64x winner. Whether or not this would be considered a venture scale ‘success’ on the portfolio-level depends entirely on fund size.

But the magic of compounding only reveals itself with patience.

Let’s re-cut the analysis and consider a new narrative — what if the investor held until today?

19-years is the gap between 6x and 1,658x. To contextualize — that is the difference between returning a $75M fund, and returning the entire AUM of Bessemer Venture Partners. We underrate how fast value can compound when you simply let it keep rolling.

Sequoia’s 2021 pivot to an evergreen “Sequoia Capital Fund” is a useful signal: one master pool now feeds its vintage-dated seed, venture, and growth sleeves while holding public positions indefinitely. In other words, permanent capital with vintage accountability.

I suspect more franchises will adopt similar vehicles — you’re already seeing it happen with firms like Thrive Holdings. AI could prove the steepest compounding curve we’ve ever invested in, and rollup platforms only show their full power after decades of reinvestment. If you truly believe that thesis, you want to own the equity, not flip it on a ten-year clock — capital structures have to stretch.

Change Management is Harder Than You Think

Silicon Valley was built on a different mindset than what this playbook calls for.

The conventional reflex is to build from scratch, not to change an existing institution. Take NASA’s Space Launch System versus SpaceX: SLS spent a decade and billions per flight to reach orbit once, while SpaceX went from a blank sheet to Falcon 9 launches in five years and now flies weekly for under $3,000 per kilo. Yes, NASA is a public agency, but my point about battling a bureaucracy vs. green-field still stands: Musk did not try to use his influence to overhaul NASA from within — the SpaceX team rewrote the entire playbook from the ground up (vertically integrated factories, fail-fast culture, etc).

It seems to have worked moderately well:

Founders expect the pain of going from zero to one on product but few are prepared for the grind required to drag legacy teams, processes, and politics out of the past. The resistance is mentally draining and often irrational — most talented builders probably don’t want to spend 18-months untangling middle-management sabotage. Shipping an LLM prototype can be a week of work, but rewriting SOPs, retraining staff, and persuading risk, compliance, and IT can take a year. Until every acquired business runs on the same workflows, your technology advantage will not compound. You need adoption, and that is easier said than done.

Ego is the Silent Saboteur

We’ve talked about change management, but sometimes those entrenched workflows exist for good reason.

A business evolves its processes for reasons that outsiders don’t always see — regulatory quirks, supplier politics, fragile customer habits. It’s important to dig into why a business is operated the way it is. An appropriate case study is the Thrasio post-mortems and the public Chapter 11 filing. I don’t have any inside baseball, but the general consensus I’ve read is that leadership did not listen to the ex-brand operators. Leverage and frothy multiples played a role, but it seems to largely be a story of overconfidence.

I admit that AI rollups require a centralized, opinionated playbook. Someone must decide which workflows get rebuilt and which tech stack wins. But decision-making must be well-informed. The moment leadership stops listening, hubris creeps in and the flywheel stalls.

I’m biased toward the Brad Jacobs school of operating: start every integration with a listening tour. His note to Beacon Roofing’s employees is a textbook example of what I’m talking about: honour what already works, mine the frontline for ideas, then layer tech on top. Humble curiosity is a good way to operate in business (and life).

Last year I wrote that, “The largest risk that I see with this playbook is the hubris associated with thinking you can run a business better because you have the right tech stack.”

I think that is more true than I had considered.

You Need More People at the Table

In your conventional software business, you can get away with one founder. I don’t think that is realistic here. At the core of this playbook, I think you’re ultimately trying to build and operate three businesses:

A product company – ships and iterates on proprietary software

An aggregator – finds, diligences, finances, and closes deals

A process company – standardizes day-to-day operations across the acquired assets

Each leg needs an A-calibre leader with a very different background and incentive structure. I wouldn’t want to back a first deal until you already employ someone with multi-decade operational expertise to diligence and run the asset day-one. There is no substitute for scar tissue.

Even with world-class people in each box, incentives collide. Product pushes for velocity; corp dev wants to do more deals; ops hates breaking workflows twice in one quarter. Tight coupling between these three teams – shared OKRs, equity that vests on integrated EBITDA, not just closed deals or shipped features – reduces that risk but does not eliminate it.

You need world-class operators in each of these roles who understand what you’re trying to do. If you even doubt whether you have killers in any of these roles, you’re dead in the water.

AI-Native Services Businesses Often Make More Sense for Venture

When you launch a firm that’s born around agentic workflows, every email, model, and meeting transcript is captured in a clean, structured form from day one. That ‘data exhaust’ feeds the very agents that automate the next engagement, so gross margin expands with each client you serve. Because you don’t inherit legacy tech or politics, a two-person pod can handle work that used to require a 15-person team—exactly the type of nonlinear efficiency venture that investors love.

This also applies to the tradeoff between building a software business versus a services business. In the first inning of the GenAI era, founders instinctively rushed to build standalone software, but the vendor lane is now congested (Harvey, Hebbia, Rogo, Glean): everyone is pitching the same law firms, banks, and consultancies (H/T Harry). Those buyers will choose one, maybe two, systems to badge as their “AI strategy.” And then shut the door.

Services, on the other hand, remain wide-open. Incumbent firms will not rip up their pyramids just because GPT-o3 can draft a memo. But model quality is compounding toward 99%+ accuracy and when it crosses that threshold, the firm designed around agents from day one will have a structural cost advantage the old guard can’t match. Ori Eldarov lays out this argument well in ‘The Bull Case for an AI-native Investment Bank’. It’s also worth noting that the services market likely will be more fragmented. There will be a longer tail of smaller winners.

Building a new practice lets you design culture, incentives, and tooling around agents from day one. The feedback loop is immediate – ship a new model tweak on Monday, watch throughput jump by Friday. I’d bet that most technology founders would find that more energizing than trying to convince a 300-person incumbent to abandon comfortable habits forged over decades.

Plug: Sahil Patwa recently posted a few solid frameworks on when it makes sense to build an AI-Native services co versus a rollup.

‘Data Flywheels’ Are Often a Fallacy

This might be a hot take, but I think that the we’re-buying-their-data-for-the-flywheel pitch is directionally a fallacy. The data requirements to build functional agentic products in 2025 are much lower than the NLP use cases tackled in 2018. We can now fine-tune models with minimal data and get to solid MVPs. Moreover, most of the “data” you would be acquiring from a mid market business is unlabeled PDFs and ERP exports you’ll never tame.

Real leverage shows up only when you rebuild the workflow from scratch. Think OffDeal – they’re able to pipe every email, model, and call note into a single vector DB so a two-person pod can run a dozen mandates without losing context. That advantage didn’t come from raiding an old shop, it came from re-architecting one.

So be honest… when you buy an operating asset, you’re probably grabbing distribution and LTV-to-CAC arbitrage, not a magic data moat. The flywheel starts spinning after you rip out the plumbing and fight through the change-management trenches – data created post-acquisition, not pre-sale. Anyone selling you otherwise is trying to make their pitch more attractive to VCs.

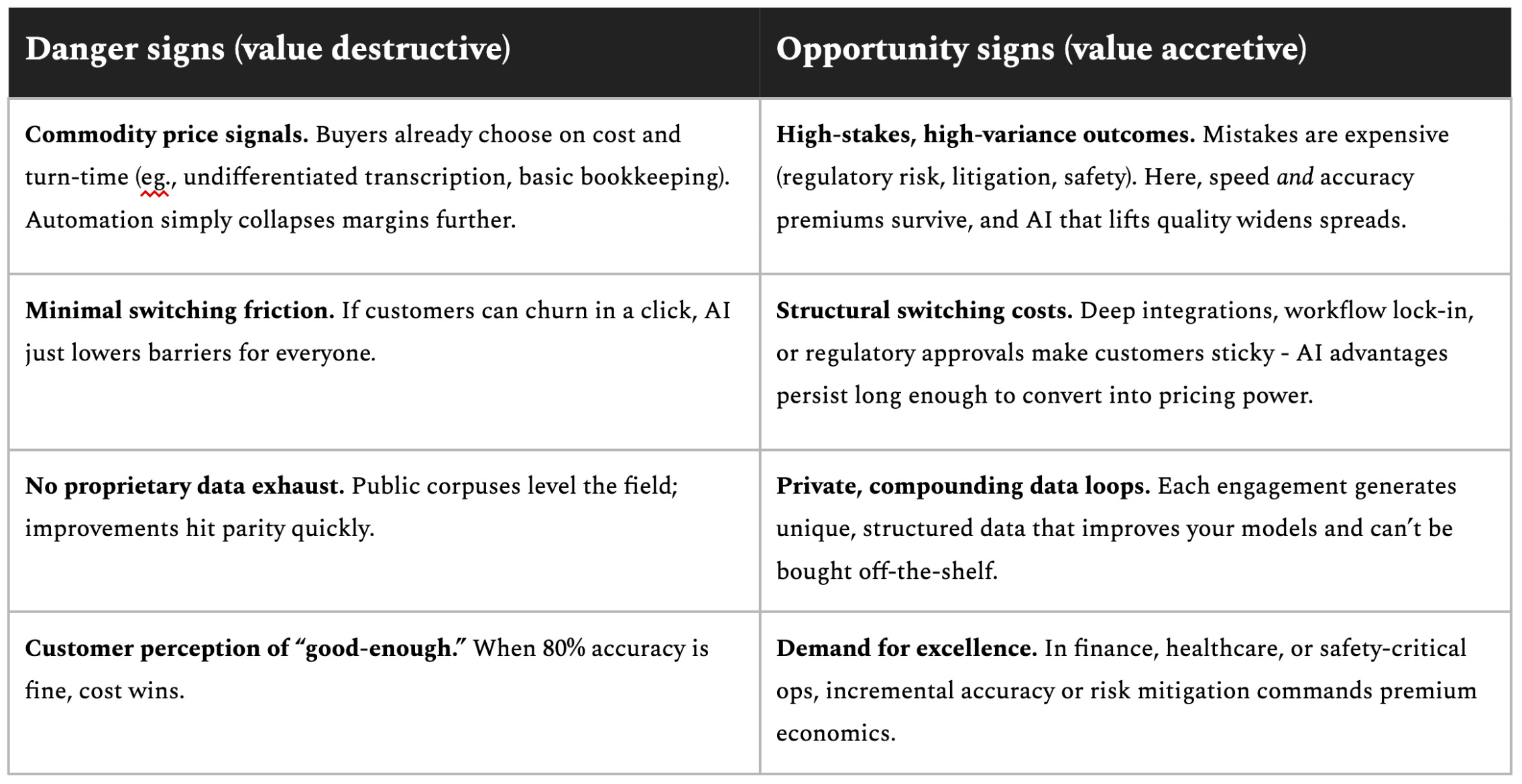

Value Accretion versus Value Destruction

AI behaves like an amplifier. In some markets it widens moats, in others it accelerates a race to the bottom for pricing. Before you lock in a roll-up thesis or an AI-native service play – you need to pressure-test the direction of value flow. I don’t have a crystal ball, but I do have a general underwriting framework that I use to keep away from the obvious meat grinders:

My thoughts here are very fluid and I’d be curious to hear how others are thinking about the durability of certain industries as AI improves.

PE is Well Positioned… With the Right Technology Partner

Alpine Investors’ 2024 scorecard is a reality check for anyone picturing an “easy” roll-up:

23,000 + deals sourced

175 acquisitions closed

$18bn AUM

That kind of sourcing volume, transaction discipline, and integration muscle is why most large-scale consolidations belong inside PE houses, not on a seed stage cap table. They already have the origination funnels, the playbooks, and the patient capital.

The one gap: turning dozens of bolt-ons into a genuinely tech-enabled platform. What PE platforms need is a forward deployed AI team that knows how to operationalize products in the messiness of real data and processes.

The execution gap lives at the intersection of messy data and real-world processes. It’s also where my team at AltaML spends most of our time. We’ve shipped more production AI workflows in finance, energy, and healthcare than almost anyone in North America. Today we’re embedding within rollup platforms and hardening their agentic processes so deal teams focus on sourcing and integration.

If you’re running (or backing) a rollup and want the tech layer to stick, let’s talk. We’re adding a handful of new partnerships this year and would love to compare notes.

Closing Thought

After a year of staying close to the metal on this, I remain a strong believer in this playbook.

The reason it remains attractive boils down to one thing – AI capabilities currently far outstrip market distribution. As long as that fact remains true, there is an arbitrage opportunity that likely represents one of the largest opportunities in technology today. Rollups are not the only way to participate in this opportunity. Figuring out how to play this game is highly dependent on the market you’re going after, and execution will take years of chewing glass, but if you can figure this out, the upside is enormous.

See you out there.

Thank you Cory Janssen, Kenndal McCardle, Luke Sophinos, Ryan Shannon, Noah Nagle, Sahil Patwa, and Harry Wruck for your feedback on various iterations of these ideas and this blog post.

Great post! Running this playbook for North America truckload freight: www.nuvocargo.com. Would love to chat: deepak@nuvocargo.com

Great piece Evan